Key takeaways:

- If you have the means, now may be a good time to buy a house.

- It’s a buyer’s market – there are nearly 500,000 more home sellers than buyers – but housing is still largely unaffordable.

- Prices keep rising: The median U.S. home sale price hit at a record $447,000 in June, marking two-straight years of gains.

- Consumers are wary due to elevated mortgage rates, tariffs, and broad economic uncertainty.

Summer is heating up – but the housing market didn’t get the memo. Following an abnormally slow spring homebuying season, the same sluggish trends are continuing: fewer home sales, limited listings, and stubbornly high prices. Record-high unaffordability and economic volatility continue to keep most on the sidelines.

While prices could dip by the end of the year, buyers are still unwilling to spend big. So, it’s no surprise that many are wondering if now is the right time to take the leap.

In short, whether or not it’s a good time to buy a house boils down to if it’s a good time for you to buy a house. Let’s dive a bit deeper into today’s market trends to help you answer: “Should I buy a house now or wait?”

From Redfin’s Chief Economist

“Nationally, now is a good time to buy, if you can afford it. Prices keep climbing, but there is also significantly more inventory, giving buyers an upper hand in negotiation. A volatile economy is making everyone uneasy, though, and local markets vary widely. Buyers serious about making offers should consult a local agent and be confident in their finances and future income.” – Daryl Fairweather, Redfin Chief Economist.

What buyers need to know about the housing market

Here are some key market trends to keep an eye on and help you make an informed homebuying choice.

House prices are high but could fall soon

The median U.S. sale price is $447,000 – up 1% from a year ago. House prices have posted year-over-year gains for two straight years and are 31% higher than they were in 2020. Monthly housing costs have sat in record territory for months.

But now, with affordability hitting new lows, more buyers are stepping back, causing inventory to grow and easing upward pressure on prices. Redfin predicts that these trends will actually push house prices down by the end of the year, making homebuying more affordable because wages are expected to rise.

If you’re planning to buy, moving soon could help you take advantage of lower competition.

>> Read: Redfin’s 2025 Housing Market Predictions

Mortgage rates are elevated and volatile

As of July 21st, daily average 30-year fixed mortgage rates sit at 6.78% – slightly down from last week. The job market continues to outperform expectations, which is keeping rates relatively high. Looming tariffs and an uneasy economy are also contributing.

“Economic uncertainty means buyers should expect mortgage rates to remain volatile for the foreseeable future,” cautioned Chen Zhao, Head of Economics Research at Redfin. “Unless all tariffs since inauguration day are called off, or inflation doesn’t materialize, rates are unlikely to fall. That being said, any dips will be a welcome break for homebuyers.”

Redfin predicts that mortgage rates will hover between 6-7% this year.

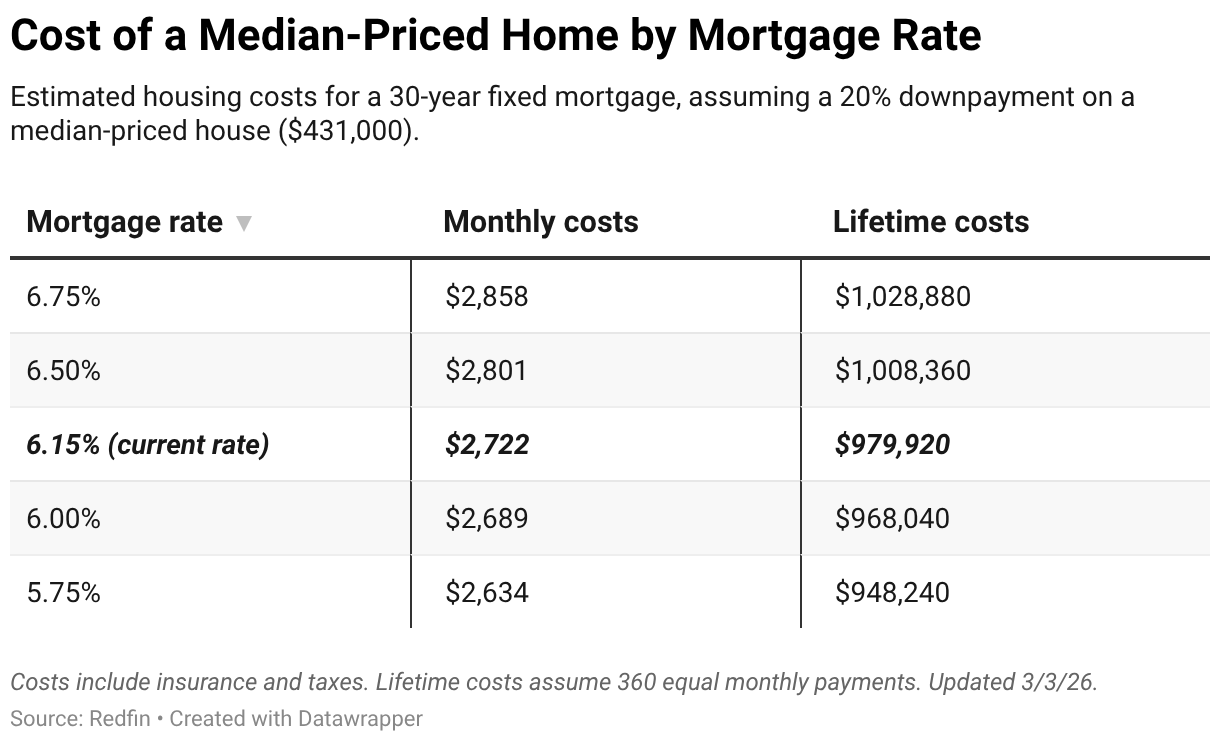

How mortgage rates affect housing costs

Mortgage rates are important for buyers because they directly translate to monthly housing costs. The higher the rate, the more you pay every month. If rates drop, you can save tens of thousands over the lifetime of your mortgage.

Let’s see how your monthly payments change with different rates, using data from our Mortgage Calculator.

Buyers have the upper hand

It’s a buyer’s market for the first time in years: Housing inventory is rising across the country – especially in the South – giving buyers more negotiating power. However, supply is still very low in parts of the Midwest and East Coast, putting sellers in charge and pushing up prices.

In general, high costs are keeping buyers on the sidelines and freezing home sales, especially among younger generations: Nearly a quarter of Gen-Z and Millennial homebuyers used family money to help with down payments, demonstrating how difficult the market is.

Let’s dive a bit deeper into the data and look at two key indicators.

Inventory is at a five-year high

There are more homes for sale in the U.S. today than there have been since the start of the pandemic – nearly $700 billion worth. Florida and Texas have the most homes on the market today, by far. This is the primary driver behind today’s buyer’s market.

Housing inventory is rising because more sellers are listing their homes than buyers are buying them, with some of the largest increases in disaster-prone areas like Florida. In fact, local Florida experts believe a market correction – where home prices fall to better reflect local incomes and demand – could be in store.

Buyers who can afford today’s market may be in a better position to receive concessions. However, a growing number of sellers are now reconsidering because they’re realizing they can’t sell for as much.

Demand is near an all-time low

Even with more homes on the market, buyer demand remains sluggish due to high housing costs and economic uncertainty – especially in markets like Austin and Tampa. For buyers who have the budget, this could be a good time to enter the market, as sellers may be more open to negotiation.

Still, there are exceptions. In some Midwest cities like Dayton and Detroit, strong demand for affordable homes is pushing prices up and putting sellers in charge.

>> Read: How to Sell Your House in 2025: A Comprehensive Guide

Inflation could rise

Critical to the housing market, the Fed and economists are concerned that inflation could rise, which would impact mortgage rates and affordability.

There is uncertainty around how much tariffs will affect inflation, though, with a few economists beginning to believe it may not end up playing a large role. Most experts still believe that tariffs will raise prices on nearly all goods.

Inflation has major implications for buyers. Most importantly, it can lead to higher house prices and mortgage rates, and stretch budgets further. If inflation does tick back up, borrowing could get more expensive, making now a smart time to lock in a rate before that happens.

>> Read: A Housing Market Under Donald Trump: What It Could Mean for Buyers, Sellers, and Renters

How to buy in an uncertain economy

With tariffs, economic whiplash, and volatile mortgage rates, many buyers are wary of getting into the market. Here are a few tips from our economists about navigating this shifting landscape.

- Stick to your budget: This isn’t the time to stretch financially. With recession odds hovering around 50% and economic uncertainty rising, make sure you have enough in savings to cover mortgage payments if your income changes.

- Negotiate, negotiate: The market favors buyers, so use your leverage. There’s more inventory, and sale prices are increasingly coming in below asking.

- Be smart about rates: Mortgage rates are unpredictable. Shop around, compare lenders, and ask about “float down” options if rates drop significantly after you lock in. You can always refinance later if needed.

- Sell before you buy: If you own a home, consider selling it first. It will give you a clearer budget and help you avoid the risk of carrying two mortgages.

>> Read: How to Buy, Sell or Rent a Home Amid Economic Uncertainty

Personal considerations: Are you ready to buy and own a house?

When deciding whether to buy a home in today’s climate, you’ll want to think beyond market conditions and focus on your individual circumstances. Here are some personal considerations to keep in mind.

Financial health

Take stock of your current savings, credit score, and debt levels. Can you afford a house? Or does renting make more sense?

Housing is a long-term commitment, so you’ll want a solid emergency fund – ideally covering 3 to 6 months of expenses – for maintenance and unexpected costs.

Monthly budget

Determine how a mortgage payment at today’s rates might impact your lifestyle. Make sure you can comfortably handle monthly payments, property taxes, insurance, and other homeownership expenses.

Job and location stability

Buying a house makes sense if you plan to stay put for several years. A stable job or reliable income is crucial to avoid financial strain, especially if home prices or interest rates rise further.

Choosing your location is also essential. Is your potential home prone to flooding, wildfires, or other climate risks? This is especially important today, as insurers continue dropping homeowners at alarming rates.

Personal goals and timelines

Think about life events, like starting a family, retiring, or relocating. These factors can make owning a home either more appealing or potentially riskier if you need to move soon.

Lifestyle preferences

Homeownership comes with ongoing responsibilities, like maintenance, repairs, and property taxes. Ask yourself if you have the time, resources, and a desire to handle them.

>> Read: Am I Ready to Buy a House? 8 Questions to Help You Decide

So, is now a good time to buy a house?

If you have the means and are ready to own a home, now is a good time to buy a house. Prices and rates are high, and with today’s economy, it’s hard to know what they’ll look like down the line. Waiting for rates to drop leaves you at risk of competition among buyers and subsequent price hikes from sellers.

In a market this unpredictable, the best approach is to be prepared. Know your budget, connect with an agent, get preapproved, save big with Rocket Mortgage, and move quickly if the right home comes along. The longer you wait, the more competition you’ll see – especially if prices fall by the end of the year.

Source link